The term micromobility, for most, conjures up the image of electric scooters and bike-sharing programs that have become ubiquitous across most of Europe and much of North America, or electric mopeds and vespas in the APAC region and in Southeast Asia. Recent years have seen massive funding rounds raised by electric scooter and moped sharing innovators as well as significant press coverage as some of these same innovators face significant financial challenges.

This micromobility boom of e-bikes and e-scooters has failed to spread across much of the African continent. An examination of micromobility across Sub-Saharan Africa reveals a demand for markedly distinct products as well as supply and demand challenges and opportunities.

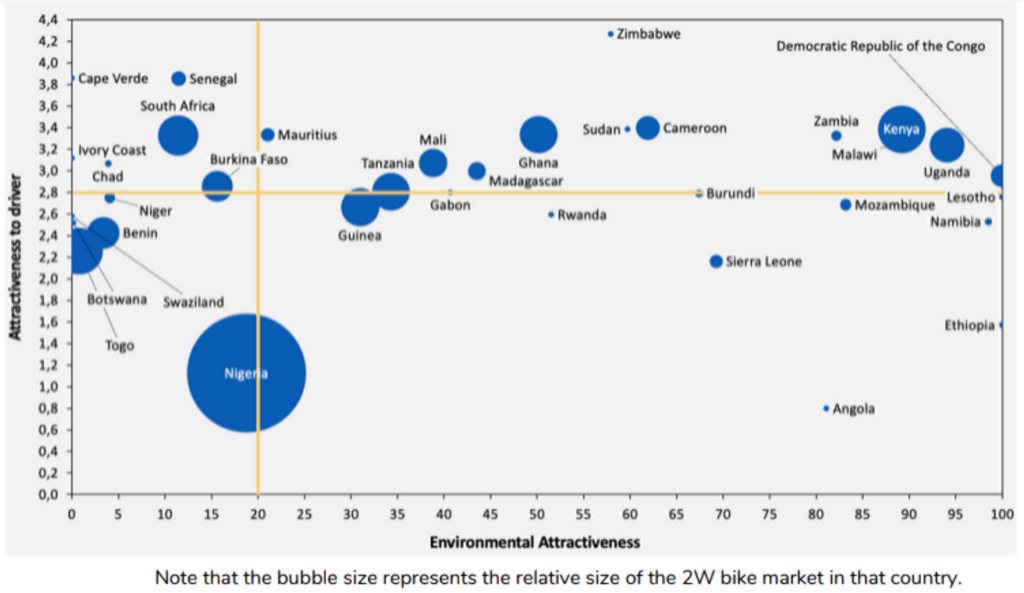

Map of Countries by Economic and Environmental Attractiveness for E2W Market

Demand for Two-wheel EVs

Motorcycles are increasingly popular in Sub-Saharan Africa, growing from about 5 million registered two-wheelers in 2010 to over 27 million in 2022. A significant driver of this growth is due to the economic opportunities that two-wheeled vehicles create for drivers, primarily as taxis and cargo and food delivery. Estimates suggest that up to 80-90% of two-wheelers are used for commercial purposes across the region.

As fuel prices rise and fuel subsidies are withdrawn, electric two-wheelers (E2W) are reaching total cost of ownership (TCO) parity with their ICE counterparts. According to some innovator investments, the cost of charging or battery swapping can reduce daily driver fuelling costs by up to 50%. As most customers are commercial drivers and put high mileage on their vehicles, these cost calculations can significantly impact their overall income.

Advantages of Local Design

While there are a plethora of low-cost e-bikes and scooters available for import to Sub-Saharan Africa (namely from China or Japan), these products do not meet the local needs of most Sub-Saharan Africa micromobility markets. These imported vehicles are not durable or agile enough to deal with difficult road conditions, nor do they have the cargo capacity required by many commercial drivers.

Local innovators have identified this gap in the market for E2W vehicles with sufficient durability, cargo-capacity, and the range to meet the needs of commercial drivers and are developing innovative solutions to overcome key market barriers.

Market Challenges: Access to Financing and Grid Stability

One of the main challenges facing e-mobility innovators in Sub-Saharan Africa markets is the high up-front cost of EVs compared to ICE (Internal Combustion Engine vehicles) in markets where consumer purchasing power is quite low. E2W can cost up to double the price of a comparable ICE motorcycle, a significant barrier for the majority of end customers who have limited cash availability and prohibitively high interest rates in some countries (standard interest rates in Ghana reached over 30% in December of 2023), complicating vehicle financing through loans.

Additionally, electricity access and grid stability vary widely between countries and regions, posing a significant challenge to the development of EV charging infrastructure as many local grids cannot accommodate the additional load of EV charging. Local charging infrastructure is critical to EV adoption, particularly for commercial riders, the majority of two-wheel vehicle customers.

Battery Swapping and Batteries-as-a-service Address Local Challenges

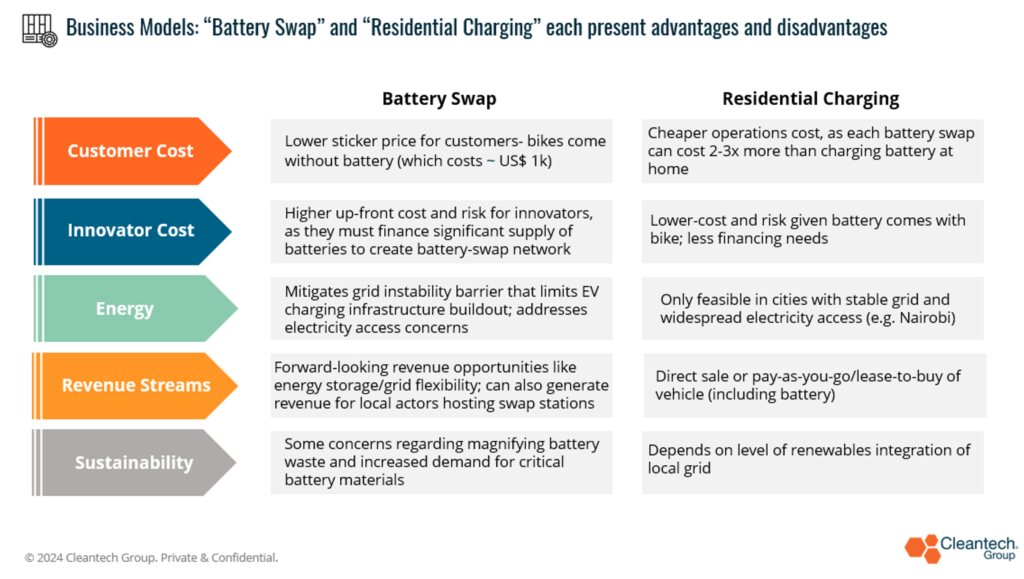

To address these challenges, start-ups are establishing innovative business models, namely battery swapping and battery-as-a-service, taking advantage of local EV tax incentives and reductions, and engaging with local financing actors to establish flexible payment options for customers. The batter-as-a-service business model (exemplified by E2W innovators such as Ampersand and Rwanda Electric Motors) allows customers to purchase the vehicle without the battery (the most expensive element of the vehicle).

Instead, the innovator provides a subscription service renting out the battery on a daily, weekly, or monthly basis and provides access to a network of battery swapping stations. The battery-as-a-service business model reduces the barrier of up-front costs for customers and creates opportunities for local businesses to engage in the e-mobility ecosystem by hosting battery swap locations.

Many innovators have adopted battery swapping even if the battery is included in the vehicle price. Notable exceptions include Roam Electric (Kenya) and Solar Taxi (Ghana) which offer a combination of public and residential charging. The operational cost of battery swapping subscriptions can be significantly less expensive than conventional refuelling costs of ICE two-wheelers.

Between lower maintenance costs and battery swapping vs. refuelling costs, some innovators estimate the commercial drivers can save between 30% – 50% by switching to E2Ws. In addition, as battery swapping stations do not incur the peak energy demands of EV charging stations, e-mobility innovators side-step the challenge of grid reliability and establish extensive battery swapping stations to support local drivers. Some innovators (e.g., ArcRide) are able to accommodate more than one battery in a single vehicle to increase range.

Looking Forward

- An extensive e-mobility ecosystem is developing around EV financing and expertise — crucial services to increase EV adoption.

- Innovators are partnering with asset financing organizations (e.g., Watu, Jali) to provide flexible loan and financing as well as lease-to-own payment options.

- Public and private sectors are cooperating to establish maintenance and manufacturing expertise — particularly education courses for technicians and partnerships between innovators and private mechanics to provide vehicle maintenance and warranties.

- Local and regional tax incentives for local production and assembly of electric vehicles as well as lowered tariffs for EV charging will be critical to bring down production costs for innovators as they increase commercial production capacity.

- Equity financing is now key for innovators to scale commercial production and succeed in increasingly crowded markets (e.g., Kenya, Nigeria). Less risk-averse investors (e.g., Persistent Energy) are leading the charge on investment in early-stage innovators in these markets.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- PlatoHealth. Biotech and Clinical Trials Intelligence. Access Here.

- Source: https://www.cleantech.com/e-mobility-in-sub-saharan-africa-electric-two-wheelers-gaining-momentum/